Most people don’t think twice about car insurance until they’re standing in a lot, staring at a surprisingly cheap vehicle with a history they can’t quite explain. You search the VIN, and there it is a salvage title. Suddenly, the price makes sense. But then comes the real question: can you even get auto insurance for salvage vehicles, and if so, how does that actually work?

This isn’t some edge-case scenario. Thousands of Americans buy salvage or rebuilt title cars every year, often to save money on a reliable daily driver. The insurance side of it, though, trips people up constantly. So let’s walk through exactly how it works, what to expect, and how to avoid the costly mistakes most buyers don’t see coming.

What Is a Salvage Vehicle, Really?

Before getting into the insurance part, you need to understand what a salvage title actually means because a lot of people confuse it with a rebuilt title, and those two are treated very differently by insurers.

A salvage title is issued by your state when an insurance company declares a vehicle a total loss. That happens when the cost to repair the car is more than its actual cash value (ACV), usually when damage reaches 60% to 90% of the car’s worth depending on the state. The car gets pulled from the road, the title gets branded as salvage, and from that point on it cannot be legally registered or driven.

Here’s the thing people don’t always hear: a salvage title car is not permanently off the road. It can be repaired, inspected, and re-titled as a rebuilt title vehicle. Once that happens, it becomes eligible for registration again, and that’s where auto insurance for salvage vehicles starts to become a real conversation.

If you’re curious about how a car’s title status affects your overall coverage obligations, it helps to first understand whether you’re even required to carry auto coverage in your state.

The Key Difference: Salvage Title vs. Rebuilt Title

This is the most important distinction in the entire topic, and most guides skim over it. Here it is, plain and simple:

| Title Type | Can You Drive It? | Can You Insure It? |

|---|---|---|

| Salvage Title | No illegal on public roads | No not insurable as-is |

| Rebuilt Title | Yes after passing state inspection | Yes with limitations |

You cannot get auto insurance for salvage vehicles that still carry a salvage title. Full stop. No insurer in the US will write a policy on a car that hasn’t been repaired and inspected. The reason is straightforward: the car isn’t safe to drive, and insurers won’t cover something they can’t assess for roadworthiness.

Once the car is properly repaired and passes your state’s inspection, the DMV issues a rebuilt title. At that point, auto insurance for salvage vehicles becomes possible but the coverage options are different from what you’d get with a clean title car.

Why Insurers Treat Rebuilt Title Cars Differently

Think about it from the insurer’s point of view. A car that was once declared a total loss has a documented history of serious damage. Even after repairs, there’s always a question: were those repairs done correctly? Was the frame fully straightened? Are the airbags properly functional again?

Insurance companies can’t always answer those questions with certainty, which is why they limit what they’ll offer. The concern isn’t theoretical either. A rebuilt car might look perfect on the outside while still having issues with its structural integrity or safety systems that don’t show up until an accident happens.

Because of this, insurers often treat rebuilt title vehicles as a higher-risk category, similar to how they’d view a driver with a checkered record. The car’s past follows it everywhere, including onto every insurance application you fill out.

What Coverage Can You Actually Get?

Here’s where things get practical. When you’re shopping for auto insurance for salvage vehicles that have been rebuilt, these are the coverage types you’ll encounter:

Liability Coverage

This is the most widely available option for rebuilt title vehicles. Almost every insurer that will touch a rebuilt car will offer liability coverage. It covers damage you cause to other people and their property not your own car. It’s also the minimum required by law in nearly every state.

Uninsured Motorist Coverage

Most states require this alongside liability, and it’s generally available for rebuilt title vehicles. It protects you if you’re hit by a driver with no insurance.

Personal Injury Protection (PIP) and Medical Payments

These cover your own medical costs after an accident. Availability varies by insurer and state, but most carriers that accept rebuilt titles will include these.

Comprehensive and Collision Coverage

This is where it gets harder. Many insurers flat-out won’t offer comprehensive or collision on a rebuilt title vehicle. Those who do will typically only cover around 80% of the car’s assessed value and that assessed value is already lower because of the title history. A rebuilt car is generally worth 20% to 40% less than a comparable clean title vehicle, according to automotive valuation standards. So even if you get full coverage, the payout on a claim will be noticeably smaller.

Step-by-Step: How to Get Auto Insurance for a Salvage Vehicle

If you bought a salvage car and want to get it road-legal and insured, here’s exactly how the process works:

Step 1: Complete All Necessary Repairs

Every repair must be done to your state’s standards. Keep receipts and documentation for everything. Insurers and inspectors will ask for this paper trail.

Step 2: Get a Certified Mechanic Inspection

Many states require a statement from a licensed mechanic certifying that the vehicle is roadworthy. This isn’t optional it’s part of getting the rebuilt title issued.

Step 3: Pass Your State’s Salvage Inspection

Your state DMV or a designated inspection station will physically check the vehicle. They’ll look at structural components, safety systems, lighting, brakes, and more. Each state has its own threshold for what passes.

Step 4: Receive Your Rebuilt Title

Once the inspection is cleared, the DMV issues a rebuilt title. The salvage brand stays on the title permanently that history never disappears but the rebuilt designation means the car is now road-legal.

Step 5: Shop for Insurance with the Right Documentation

When you start looking for auto insurance for salvage vehicles, bring everything: the rebuilt title, repair receipts, the mechanic’s certification, and the inspection report. Insurers who accept rebuilt title vehicles will want to see this.

Step 6: Compare Multiple Carriers

Not every insurer will take your application. Some will offer liability only. A handful will offer more complete coverage. You’ll need to shop around, and that process genuinely takes more time than insuring a clean title car. Don’t settle for the first quote.

Understanding how to switch car insurance can actually help here you may need to move between carriers if your current one won’t cover a rebuilt vehicle.

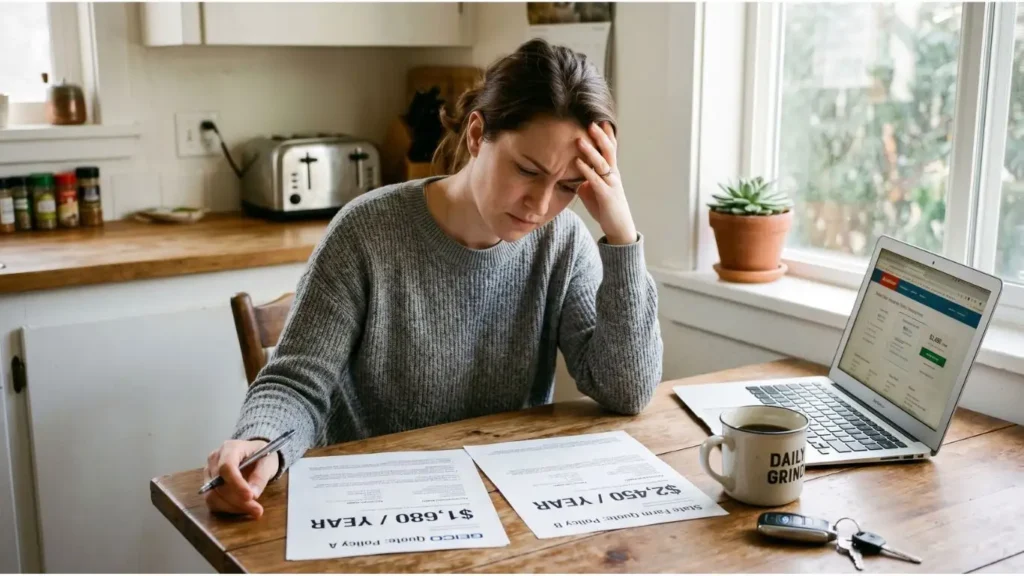

How Much More Does It Cost?

Expect to pay more. That’s the honest answer. Auto insurance for salvage vehicles that have been rebuilt typically runs 20% to 40% higher than comparable coverage on a clean title car. On an annual basis, that can add anywhere from $180 to $500 or more depending on your state, coverage level, and the vehicle itself.

The premium increase reflects the insurer’s uncertainty about the car’s true condition and its lower resale value. If they have to pay a claim on a rebuilt vehicle, their exposure is harder to calculate, so they price that risk into the premium.

Some ways to offset the higher cost:

- Carry a higher deductible to bring the monthly premium down

- Stick to liability-only if the car’s value doesn’t justify full coverage

- Bundle with another policy like renters or home insurance

- Look at smaller regional carriers or specialty insurers who are more comfortable with rebuilt title vehicles

What Happens During a Claim?

This is something most articles don’t explain well, and it matters. If you file a claim on a rebuilt title vehicle especially a collision or comprehensive claim the adjuster will try to determine whether the damage is new or pre-existing from the original incident that caused the salvage designation.

Since the vehicle already had documented major damage in its past, it’s harder for the insurer to separate old from new. This is one reason some carriers refuse to offer physical damage coverage on rebuilt vehicles at all. For those who do, the payout will reflect the car’s current diminished market value, not what you paid for repairs.

Also worth knowing: if a rebuilt car gets totaled again, some insurers will pay out less than you’d expect because the baseline value is already lower. It’s worth understanding your policy’s language on this before you ever need to file.

Special Cases: Electric and High-Value Salvage Vehicles

The rules above apply broadly, but certain vehicle types add another layer of complexity. Electric vehicles with salvage titles are particularly tricky because battery damage is expensive to assess and even more expensive to repair correctly. Some insurers won’t touch a rebuilt EV at all. If you’re looking at this category, it’s worth reading up on how electric vehicle insurance differs before making a purchase decision.

Similarly, high-value vehicles that went through the salvage process may have trouble finding comprehensive coverage even after being rebuilt, because the risk exposure on a claim is simply too high for many standard carriers.

One More Thing: Can You Insure a Salvage Car You Don’t Own?

This comes up more than you’d think, especially when someone rebuilds a Auto insurance for salvage vehicles that’s still in another person’s name. As a general rule, you need an insurable interest in a vehicle to insure it. That means you either own it, are making payments on it, or have some documented financial stake in it.

If you’re in that situation, it helps to understand whether you can insure a vehicle that isn’t in your name before assuming you’re covered.

Coverage Comparison at a Glance

| Coverage Type | Available for Rebuilt Title? | Notes |

|---|---|---|

| Liability | Yes, widely available | Meets state minimums |

| Uninsured Motorist | Yes, most carriers | Often required by state law |

| PIP / MedPay | Yes, most carriers | Varies by state |

| Comprehensive | Limited fewer carriers | Payout based on reduced ACV |

| Collision | Limited fewer carriers | Harder to separate old from new damage |

| Full Coverage | Rare specialty insurers | Expect 20-40% premium increase |

FAQs

Does the salvage history stay on the title forever, even after it's rebuilt?

Yes, permanently. Once a vehicle is branded as salvage by the state, that history never

disappears from the title record. When the car is repaired and passes inspection, the title

changes from "salvage" to "rebuilt" but the rebuilt designation itself signals to any

future buyer, lender, or insurer that the vehicle was once declared a total loss.

You can check the full title history of any vehicle through the National Motor Vehicle

Title Information System (NMVTIS) or a vehicle history report before purchase. There is

no legal process in the US that wipes a salvage brand from a title. Any seller claiming

otherwise is misrepresenting the vehicle, which is fraud.

Will filing a claim on a rebuilt title car be treated differently than a clean title claim?

Yes, in some important ways. When you file a collision or comprehensive claim on a rebuilt

title vehicle, the insurance adjuster faces a challenge that doesn't exist with clean title

cars: separating pre-existing damage from new damage. Because the car already had

documented major damage in its past, it's harder to prove what was caused by the current

incident versus what was left over from before.

This can slow down the claims process and in some cases reduce the payout. Insurers will

also base any settlement on the car's current actual cash value which is already 20% to

40% lower than a comparable clean title car. So even if the claim is approved without

dispute, you're working from a smaller number. Taking detailed photos of your rebuilt

vehicle's condition right after you get it insured is one of the smartest things you can

do. Those images become your baseline if a claim ever comes up.

Do all states handle salvage and rebuilt title inspections the same way?

No, and this trips up a lot of buyers. Each state sets its own threshold for what qualifies

as a total loss (anywhere from 60% to 90% of the car's actual cash value), and each state

runs its own inspection process for converting a salvage title to a rebuilt one. Some

states require a single DMV inspection. Others require separate brake, lamp, and smog

checks in addition to a structural inspection. A few states have particularly strict

requirements around rebuilt titles for flood-damaged or stolen-recovery vehicles.

What passes inspection in one state may not pass in another, which matters if you plan to

move or if you're buying a rebuilt title car from out of state. Always check your specific

state DMV's requirements before purchasing, not after. The car's previous inspection in

another state does not guarantee it will pass yours.

Is it worth buying a rebuilt title car, or do the insurance and resale downsides outweigh the savings?

It depends entirely on why you're buying it and how well the repairs were done. The typical

price discount on a rebuilt title car runs 20% to 40% below market value for a comparable

clean title vehicle. That's real money. But that discount comes with three ongoing costs

most buyers don't fully calculate upfront: higher insurance premiums, lower resale value

when you eventually sell, and a narrower pool of insurers willing to cover the car at all.

If you're buying for personal, long-term use and you've had an independent mechanic

inspect the vehicle before purchase, a rebuilt title car can make financial sense

especially if you're keeping liability-only coverage and the car's value doesn't justify

full coverage anyway. If you're buying it expecting to resell it in a few years, the math

gets harder. The title history follows the car to every future transaction, and buyers

discount rebuilt title vehicles heavily. The savings at purchase rarely come back at sale.

The Real Bottom Line

Auto insurance for salvage vehicles is possible, but it requires more work, more documentation, and more patience than standard car insurance. The process isn’t impossible people do it successfully every day but you have to go in knowing the rules.

The car cannot be insured with a salvage title. It has to be repaired, inspected, and converted to a rebuilt title first. Even then, your coverage options will be narrower and your premiums will be higher than what you’d pay on a clean title vehicle. Liability coverage is almost always available. Full coverage is a much harder find.

The savings you get buying a salvage vehicle can absolutely be worth it but only if you factor in what insurance will actually cost you on the back end. Before you sign anything on a salvage car purchase, make sure you understand what your total cost of ownership looks like, including the insurance side of the equation.

And if at some point you’re adding this car to an existing policy, be prepared for the insurer to ask questions, possibly require a new inspection, and potentially require a separate rider or policy. That’s normal for auto insurance for salvage vehicles, and knowing it upfront means fewer surprises when it matters most.

For further context on how state-mandated coverage requirements interact with non-standard vehicle titles, the Insurance Information Institute maintains updated guidance that is worth reviewing before you commit to a purchase.