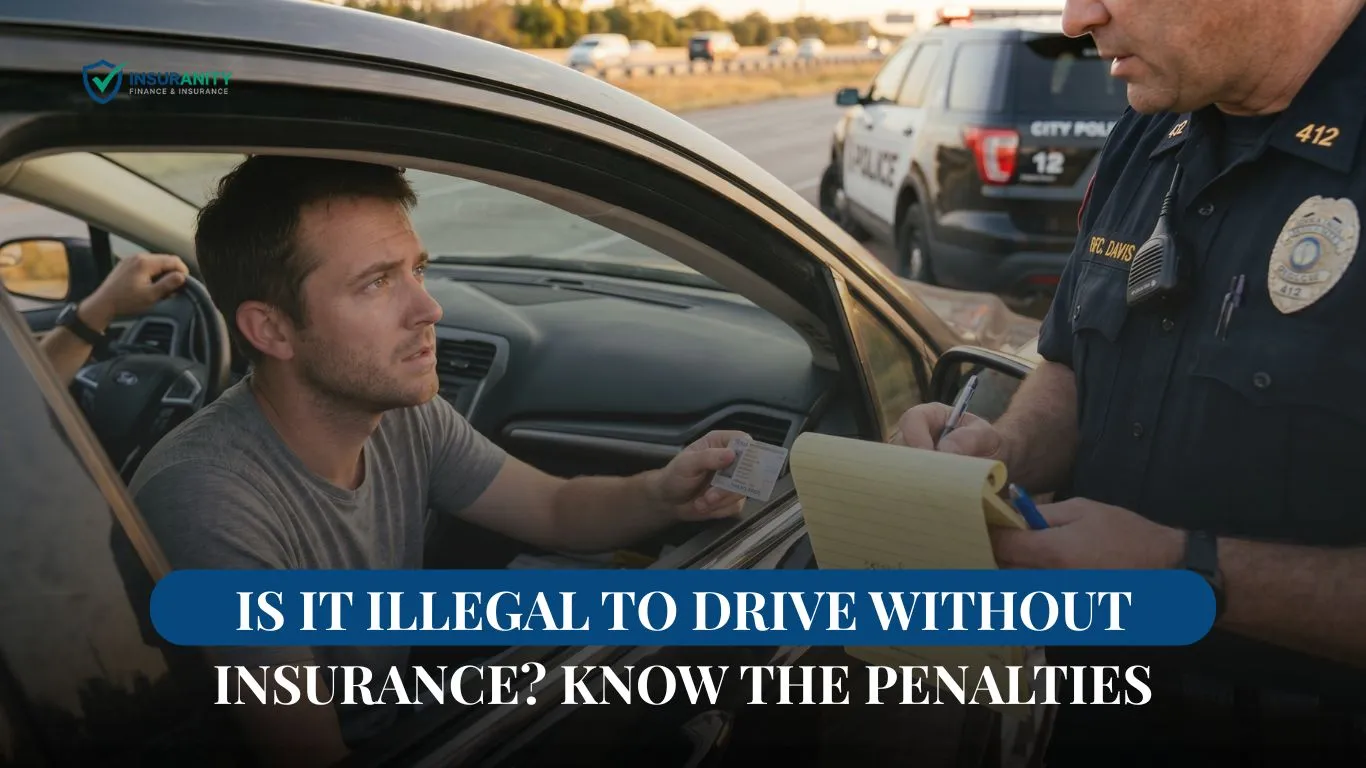

Picture this: you’re running late for work, your insurance lapsed three days ago because the auto-pay card expired, and a police officer flips on the lights behind you. Your stomach drops. That two-mile drive just turned into a possible court date, a suspended license, and a fine bigger than your monthly rent.

This happens every day across the country. And the question on most people’s minds in that moment is the same one you’re probably here for. Is It Illegal To Drive Without Insurance? In almost every state, yes. New Hampshire is the only state that doesn’t flat-out require it, and even there, you have to prove you can pay for any damage you cause. So the short answer is simple. The full answer, with all the fines, license suspensions, and weird state rules, is what most drivers don’t know until it’s too late.

Let’s walk through it the way I’d explain it to a friend over coffee.

The Short Answer Most People Need

Is It Illegal To Drive Without Insurance? Yes, in 49 out of 50 states. New Hampshire is the lone holdout, and Virginia used to let drivers pay a fee to skip coverage but ended that program in 2024. Every other state requires you to carry at least liability insurance before you put the key in the ignition.

Liability insurance is the bare-minimum coverage. It pays for the other driver’s car and medical bills if you cause a crash. It doesn’t fix your own car. It doesn’t pay your own hospital bills. It’s the floor, not the ceiling.

So why is it illegal to drive without car insurance? Because the math is brutal without it. A single fender-bender at a stoplight can cost twenty thousand dollars by the time the hospital, body shop, and tow company are done sending bills. Most people don’t have that kind of cash sitting around. Insurance is the system states use to make sure innocent victims actually get paid.

What Happens The Moment You Get Caught

Let me tell you about a guy I’ll call Marcus. He let his policy lapse for six weeks while job hunting. One Tuesday morning, he rolled through a yellow that turned red and got pulled over. The officer asked for the license, registration, and proof of insurance. Marcus had two out of three.

Here’s roughly what happened next, and what tends to happen to anyone in the same spot:

- The officer runs your plate. Most states now have electronic systems that flag uninsured vehicles in real time. They knew before he even handed over his license.

- You get a citation. This is the ticket itself. The amount depends on the state and whether it’s your first offense.

- Your license can be suspended on the spot. In several states, the officer can take the physical card right there.

- Your car can be towed. Tow fees stack up at fifty to one hundred dollars per day until you sort things out.

- You get a court date. First offenders often catch a break. Repeat offenders rarely do.

Marcus paid a $675 fine, lost his license for thirty days, and had to file something called an SR-22 for the next three years. That last one is what really hurt. An SR-22 isn’t a type of insurance. It’s a form your insurance company files with the state saying you have coverage, and it tags you as high-risk. His premiums tripled.

State-by-State Reality Check

Penalties swing wildly depending on where you live. A first offense in one state is a $25 ticket. In another, it’s a misdemeanor with possible jail time. Here’s a snapshot of how things look in the biggest states people ask about.

| State | First Offense Fine | License Suspension | Jail Possible? |

|---|---|---|---|

| California | $100 to $200 | Yes, until proof shown | No |

| Florida | Up to $500 | Up to 3 years | Rare, repeat only |

| Texas | $175 to $350 | Possible | Yes, repeat only |

| Ohio | License suspension | Up to 90 days | No |

| Virginia | $600 minimum | Yes | No |

California

Is it illegal to drive without insurance in California? Yes. Vehicle Code Section 16029 makes it a civil offense. First-time drivers usually pay between $100 and $200, plus penalty assessments that can push the total past $450. Get caught a second time within three years, and the fine doubles, your car gets impounded, and your license gets suspended for a year. California also requires you to carry proof of insurance every single time you drive, even on the way to buy groceries.

Florida

Is it illegal to drive without insurance in Florida? Florida is unusual. It uses a no-fault system, which means every driver must carry Personal Injury Protection and Property Damage Liability. If you let coverage lapse, the state will suspend your license and registration for up to three years. The reinstatement fee starts at $150 and climbs to $500 for repeat offenders. You also have to file SR-22 paperwork. This is where the real cost lives, because that filing flags you for higher premiums for years.

Texas

Is it illegal to drive without insurance in Texas? Yes, and the state takes it seriously. First-offense fines run between $175 and $350. Second offenses can hit a thousand dollars. Your car can be impounded for up to 180 days, and storage fees rack up at $15 a day. That’s $2,700 just to get your car back. Texas also adds a $250 annual surcharge for three straight years on top of everything else.

Ohio

Is it illegal to drive without insurance in Ohio? Yes. Ohio doesn’t usually issue a fine for a first offense. Instead, it goes straight for the license. Your driving privileges get suspended for ninety days, and you need to file an SR-22 along with paying a $100 reinstatement fee. Second offenses bump the suspension to a year. Third offenses bring two-year suspensions and possible vehicle plate impoundment.

Virginia

Is it illegal to drive without insurance in Virginia? It is now. Virginia used to allow drivers to pay an uninsured motor vehicle fee of $500 per year and skip insurance entirely. That program ended in mid-2024. Today, driving without coverage means a $600 statutory fee, license suspension, and SR-22 filing for three years. The state did not soften the penalties when it removed the opt-out fee.

The Hidden Costs Nobody Talks About

The ticket is just the entry fee. Here’s what actually drains your bank account over the following years.

Sky-high premiums

Once you’ve been flagged as uninsured, insurance companies charge you between 50% and 90% more than a clean driver. That extra cost lasts three to five years.

SR-22 filing fees

Every state that requires this charges your insurer a fee, which gets passed to you. Plan on $25 per filing, plus the higher policy rates.

Reinstatement fees

Most states charge between $75 and $500 to get your license back, separate from the original fine.

Court costs

If your case requires an appearance, expect a few hundred dollars in court fees on top of everything else.

Lost wages

No license means no commute. Many people end up taking unpaid time off or relying on family for rides for weeks.

When you add it all up, a single uninsured ticket often costs $3,000 to $8,000 over three years. That’s not counting what happens if you actually crash a car while driving uninsured.

What Happens If You Crash With No Insurance

This is where things get nightmarish. If you cause an accident without coverage, you are personally on the hook for every dollar of damage. The other driver’s medical bills. Their car. Lost wages if they can’t work. Pain and suffering if it goes to court.

A friend of mine totaled someone’s SUV at a four-way stop years ago. He’d let his policy slip the month before because money was tight. The lawsuit was settled at $43,000. He spent six years paying it off. His wages were garnished. His tax refunds were intercepted. His credit score cratered. That’s the real reason it is illegal to drive without insurance. The system is built around the assumption that you can cover what you break.

And in most states, the other driver’s uninsured motorist coverage will pay them first, then their insurance company will come after you for every penny. That process is called subrogation, and it’s relentless.

Is It Illegal To Drive Without Insurance? For drivers who lease their cars, things get even worse. Lease contracts require continuous full coverage, and a lapse can trigger contract violations on top of the legal trouble.

How To Avoid The Mess: A Step-by-Step Guide

If you’re reading this because you’re worried about a lapse, here’s the practical path forward.

Step 1: Check your current status today

Log in to your insurer’s app or call them. Confirm your policy is active, payment is current, and the coverage dates extend past today. People assume they’re covered all the time. Then their bank declined an auto-pay six weeks ago, and they never got the email.

Step 2: Set up automatic payments with a backup card

Most lapses happen because of a card expiration or a maxed-out account. Insurers will let you save two payment methods. Use both.

Step 3: Buy the minimum if money is tight

Some coverage is better than zero coverage. Even basic liability protects you from the worst-case scenario. If you’ve ever wondered how much basic liability really costs, the answer surprises most people. It’s often cheaper than two tanks of gas a month.

Step 4: Get an SR-22 immediately if your license is suspended

Don’t wait. Every day you drive without filing one is another offense, stacking on the first.

Step 5: If you can’t afford the regular market, check your state’s assigned risk pool

Every state has one. It’s designed for drivers that no regular insurer will touch.

Step 6: Never lend your car to someone uninsured

If they crash, your policy pays first. Then your rates go up. Then you might get dropped.

Step 7: If you’re storing a car and not driving it, consider a non-owner or parked-car policy

These options exist for situations where you have a vehicle but aren’t actively driving it, and they cost a fraction of full coverage.

What If You Don’t Own A Car But Sometimes Drive?

This is where people get tripped up. Is It Illegal To Drive Without Insurance even when you’re borrowing your sister’s car? Generally, the car’s insurance follows the car, not the driver. So if your sister has coverage, you’re usually fine for occasional use. But if you drive her car regularly, most insurers require you to be listed on her policy.

For people who often drive rentals, ride-shares, or borrowed cars, a non-owner liability policy makes sense. It travels with you across any vehicle you drive. Some folks who recently canceled their auto policy to save money end up needing this exact thing when they realize they still occasionally need a car.

The Quick Way To Check If You’re Covered Right Now

Pull up your phone. Open your banking app. Search the last 30 days for any payment to an auto insurance company. If you don’t see one, call your insurer before you drive anywhere else. The whole call takes four minutes.

This sounds basic, but it’s the single most common way people end up uninsured without realizing it. A bank changes your card number for fraud protection, the auto-pay fails, the email goes to spam, and three weeks later, you’re driving without coverage.

Why The Law Exists In The First Place

Why is it illegal to drive without insurance? Boil it down, and the answer is this. Cars are heavy, fast, and dangerous. The average American drives around 13,500 miles per year. Crashes happen. Without a financial system requiring drivers to take responsibility for damage they cause, victims would be left footing the bill for someone else’s mistake. The mandatory insurance system exists so that when something goes wrong, there’s money to fix it.

That logic applies to other parts of life too. Health insurance has its own version of this debate, and the rules there are very different. But the underlying idea is similar. Society wants to make sure costs don’t get dumped on innocent people.

The Insurance Information Institute keeps a running summary of state-by-state requirements if you want to verify the rules where you live. Their state guide is updated when laws change.

FAQs

Can the other driver sue me if I hit them and don't have insurance?

Yes, and they almost always will. Without insurance, there's no policy paying out for the damage, so the injured driver has to come straight at you for repairs, medical bills, and lost wages. Courts can order wage garnishment, place liens on your property, and intercept your tax refunds until the judgment is paid. Some states also allow the victim to sue for punitive damages on top of actual costs because driving uninsured is considered reckless. Most lawsuits settle between $15,000 and $75,000, though serious injury cases climb into six figures fast.

Will the police know I have no insurance before they pull me over?

In a growing number of states, yes. About 35 states now use electronic insurance verification systems that link DMV records with insurance company databases in real time. When an officer runs your plate, the system flags whether your coverage is active. States like Oklahoma, Georgia, and Mississippi were among the first to roll this out. So you can't always count on the officer not asking. Some patrol cars run plates automatically as they drive past parked vehicles, which is how a lot of uninsured drivers get spotted in the first place.

How long does a no-insurance ticket affect my insurance rates?

The bump usually lasts three to five years, depending on the state and insurer. Most companies pull your driving record every six months and adjust premiums based on what they find. A first-offense lapse can raise rates by 30% to 60%. A second offense or an accident while uninsured can double or triple them. Some insurers won't cover you at all for two to three years after a serious lapse, which forces you into the state's high-risk pool where rates are often two to four times higher than standard policies.

If I just bought a car, how many days do I have before I need insurance?

Most states require coverage the moment you drive off the dealer's lot, not weeks later. Dealers usually won't let you leave without proof of insurance because of liability concerns. If you bought from a private seller, the answer depends on your state. Some give you a grace period of 7 to 30 days to add the new car to an existing policy, but that only applies if you already have an active policy on another vehicle. If you're a brand-new driver with no current coverage, there's no grace period in any state. Driving the car home from the seller without insurance is technically a violation, even if it's just a few miles.

The Bottom Line

Is It Illegal To Drive Without Insurance? Yes. Almost everywhere. The penalties range from a small fine to thousands of dollars in fees, suspensions, and rate hikes that follow you for years. The smart move is simple. Check your policy today. Set up backup auto-pay. Carry at least the minimum required by your state. The cost of insurance is always smaller than the cost of getting caught without it, and dramatically smaller than the cost of crashing without it.

Is It Illegal To Drive Without Insurance? Plenty of people drive uninsured, thinking nothing will happen. Some go years without getting caught. The ones who do get caught, or who cause a crash, almost always say the same thing afterward. They wish they’d just paid the premium.