Imagine getting a surprise bill for $28,000 after one emergency room visit, with no insurance to soften the blow. That is the reality thousands of Americans face every year. But beyond the financial risk, a question keeps showing up in Google searches and Reddit threads alike: Is it illegal to not have health insurance?

Is It Illegal To Not Have Health Insurance? The short answer is: it depends on where you live. The long answer is what this guide is all about.

At Insuranity, we break down complex insurance topics into plain, simple language, so whether you are 16 or 60, you can walk away fully informed. Let’s go step by step.

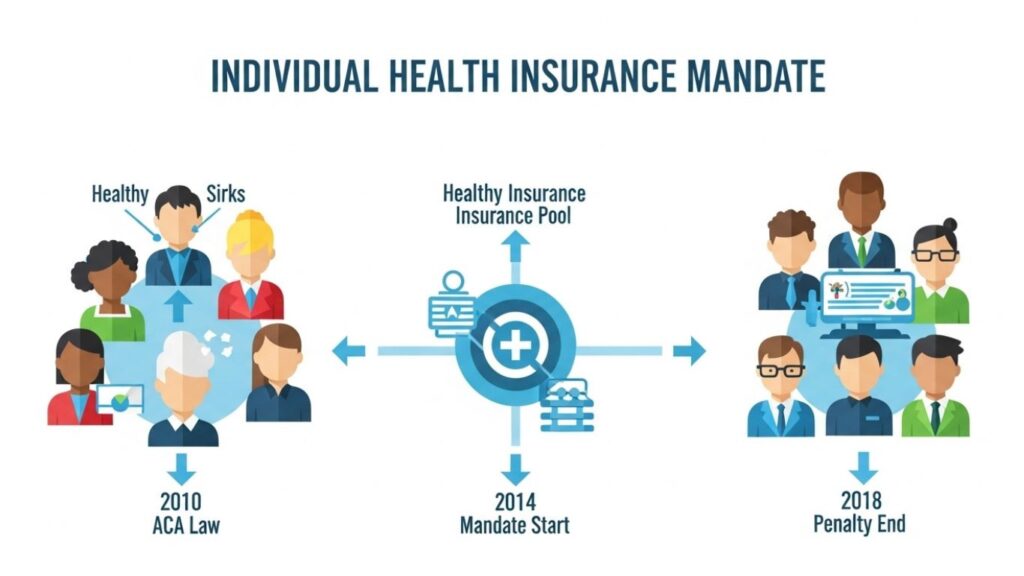

What Is the Individual Health Insurance Mandate?

Before diving into legality, you need to understand one key term: the individual mandate.

The individual mandate was a rule created under the Affordable Care Act (ACA), also known as Obamacare, signed into law in 2010. It required most Americans to carry minimum essential health coverage or pay a federal tax penalty. The goal was straightforward: get healthy people into the insurance pool so that the cost of covering sick people would spread out more evenly, keeping premiums manageable for everyone.

Think of it like a neighborhood potluck. If only sick people show up, there is never enough food. The mandate was designed to get healthy people to bring a dish too.

From 2014 to 2018, this federal penalty was actively enforced. The penalty was either a flat dollar amount or a percentage of your household income, whichever was greater, capped at the average cost of a bronze marketplace plan.

Is There Still a Federal Penalty for Not Having Health Insurance?

Here is the big shift: In 2017, Congress zeroed out the federal penalty, effective January 1, 2019.

The fee for not having health insurance, sometimes called the “Shared Responsibility Payment”, ended in 2018, meaning you no longer pay a tax penalty for not having health coverage at the federal level.

So technically, is it illegal to not have health insurance at the federal level today? No. There are no federal laws that currently impose a penalty or fine for not having health insurance. The legal wording of the mandate still exists in the ACA, but without a penalty, it has no real enforcement mechanism.

This is important to understand: the law did not disappear from the books, but it lost its teeth. You will not get a fine from the IRS for being uninsured in 2025, unless you live in one of the states we are about to talk about.

Which States Still Require You to Have Health Insurance?

When the federal government stepped back, several states decided to step forward. They created their own state-level individual mandates with real financial penalties for residents who go without qualifying coverage.

As of 2025, five states and the District of Columbia legally require residents to maintain health insurance coverage or face a state-level tax penalty. Those jurisdictions are California, Massachusetts, New Jersey, Rhode Island, and Washington, D.C. Vermont is a special case, it has a mandate on paper but does not impose a financial penalty.

So if someone asks you, “Is it illegal to not have health insurance?”, in those six places, the honest answer is: yes, it is required by law, and skipping it can cost you real money.

Here is a clear breakdown of the state-level penalties:

| State / Jurisdiction | Penalty (Per Adult) | Penalty (Per Child) | Income-Based Option |

|---|---|---|---|

| California | $900 or higher | $450 | 2.5% of income above filing threshold |

| Massachusetts | Varies by income + age | N/A (adults only) | Capped at 50% of lowest available plan cost |

| New Jersey | Varies by income + family size | Included in family calc | Based on bronze-plan cost |

| Rhode Island | $695 or higher | $347.50 | 2.5% of household income |

| Washington, D.C. | $745 or higher | $372.50 | 2.5% of income above DC threshold |

| Vermont | Mandate exists | No penalty enforced | N/A |

Penalties are calculated when you file your state tax return. Always verify current amounts with your state’s tax authority.

Step-by-Step: How to Know If You Are Required to Have Health Insurance

Follow these simple steps to understand your own situation:

Step 1: Find out which state you live in

If you live in California, Massachusetts, New Jersey, Rhode Island, or Washington, D.C., you are legally required to carry health insurance.

Step 2: Check if you qualify for an exemption

Every mandate state offers exemptions. Common ones include:

- Your income is below the state’s filing threshold

- Coverage is deemed unaffordable under your state’s rules

- You experienced a financial or personal hardship

- You belong to a qualifying religious group

- You had a short gap in coverage (usually 1 to 3 months)

Step 3: Check if your current coverage counts

Most people who have employer-sponsored group health insurance automatically satisfy state mandates. Medicare, Medicaid, and most ACA marketplace plans also qualify as minimum essential coverage (MEC).

Step 4: If you are uninsured, explore your options during open enrollment

Open enrollment for most states using HealthCare.gov ran from November 1, 2025, through January 15, 2026. If you missed it, check if you qualify for a Special Enrollment Period (SEP) due to a life event like losing a job, getting married, or moving.

Step 5: File your taxes correctly

If you were uninsured in a mandate state, you will need to report your coverage status, or pay the penalty, when filing your state income taxes.

Why Do States Still Want You to Have Health Insurance?

Is It Illegal To Not Have Health Insurance? Let’s clear something up: these state mandates are not about punishing people. They exist because individual mandates help maintain a balanced insurance pool, keep premiums from rising too quickly, and fund state healthcare initiatives such as reinsurance programs.

For example, New Jersey directs penalty revenue into a reinsurance program that has consistently lowered individual-market premiums compared to pre-mandate levels. In plain terms, the rule helps everyone, insured or not, by keeping the cost of health coverage from going through the roof.

What If You Live in a State With No Mandate?

In every other U.S. state, there is no legal requirement to carry health insurance in 2025. Residents can go uninsured without facing state or federal tax penalties. This includes large states such as Texas, Florida, New York, and Pennsylvania.

Is It Illegal To Not Have Health Insurance? So technically, if you live in Texas and you do not have health insurance, you are not breaking any law. No fine, no penalty, no IRS letter.

But here is the thing, and this is where Insuranity wants to be very honest with you, legal and smart are two very different things.

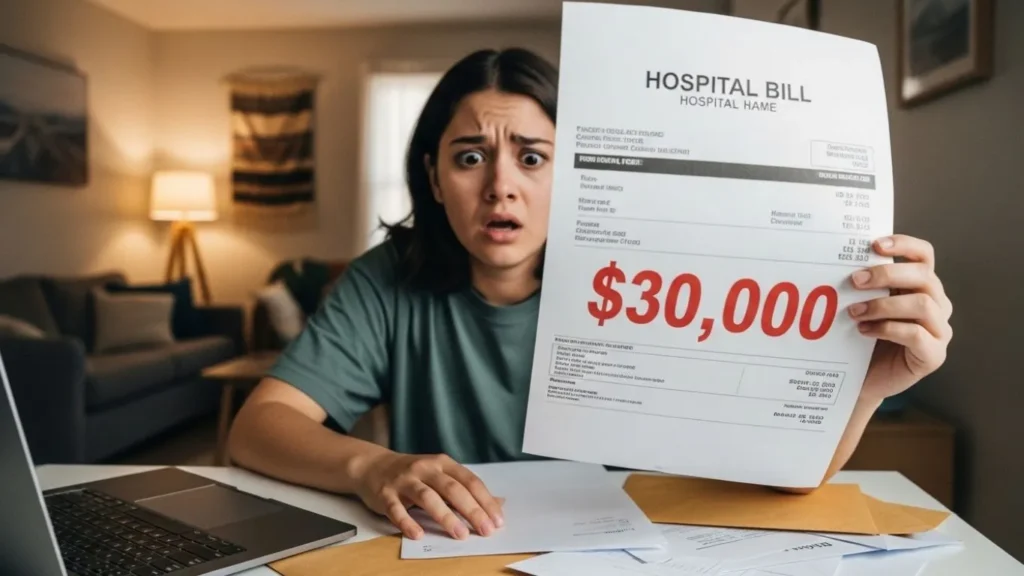

Medical debt remains one of the leading causes of financial distress in the U.S., and uninsured individuals pay substantially higher out-of-pocket costs when care is needed. A single emergency room visit averages $2,200, though costs vary by location, facility type, and treatment complexity.

Think about Sarah, a 29-year-old freelance designer in Texas who felt perfectly healthy and skipped insurance to save $280 a month. Then she broke her wrist. One ER visit, one surgery, and a short rehab stay later. She owed over $31,000. Being uninsured was not illegal in her state. But it cost her years of savings. Is It Illegal To Not Have Health Insurance

Who Can Skip Health Insurance Legally, Even in Mandate States?

Even in states that require coverage, certain people are fully exempt from the mandate. Here are the most common qualifying exemptions:

Low-income individuals

Individuals with incomes less than or equal to 150% of the Federal Poverty Level are not subject to any penalty for non-compliance in Massachusetts, for example. Other states have similar income-based thresholds.

Short coverage gaps

Most states forgive a gap of one to three months. Rhode Island’s system is notable for its detailed monthly proration, each uncovered month counts as one-twelfth of the annual penalty, but a short coverage gap of one or two consecutive months is fully exempt.

Unaffordable coverage

If the cheapest plan available to you exceeds what your state defines as “affordable” based on your income, you are typically exempt from the penalty.

Religious grounds

Members of certain recognized religious groups or health care sharing ministries may qualify for an exemption.

Hardship cases

Job loss, domestic situations, natural disasters, or other documented hardships can qualify you for a penalty waiver.

The ACA and What Changed Over the Years

Understanding the timeline makes everything clearer:

- 2010: The ACA is signed into law. The individual mandate is included to stabilize the insurance market.

- 2014: Federal mandate enforcement begins. Uninsured Americans start paying penalties on their tax returns.

- 2017: Congress, as part of the Tax Cuts and Jobs Act, sets the federal penalty to $0, effective 2019.

- 2019: The federal individual mandate penalty officially ends. No more IRS fine for being uninsured.

- 2020: California, New Jersey, and Rhode Island launch their own state mandates.

- 2025 onward: Five states and D.C. actively penalize uninsured residents. The rest of the country faces no legal requirement.

This timeline helps answer the question “is it illegal to not have health insurance” with full context. It used to be a federal issue, and now it is a state-by-state story.

Can Your Employer Be Penalized for Not Offering Coverage?

This is a part most articles skip, and it is a content gap worth addressing.

Yes. The ACA employer mandate is still very much active. Employers with 50 or more full-time equivalent employees must offer health coverage that is both “affordable”, costing less than 9.02% of household income, and provides “minimum value,” covering at least 60% of expected costs. Failing to do so can lead to penalties.

Large employer mandates mean that employers with 50 or more full-time employees face penalties of approximately $2,900 per employee annually for failing to offer adequate coverage.

So if your employer has 50 or more workers and does not offer you health insurance, that is an issue on their end, not yours. You should know your rights.

What Are Your Coverage Options if You Are Uninsured Right Now?

Whether you live in a mandate state or not, here are the main paths to getting covered:

1. ACA Marketplace Plans

Visit HealthCare.gov or your state’s marketplace. Adults with income as low as 100% of the federal poverty level may be eligible for subsidies. In 2024, you were typically eligible for ACA subsidies if you earned between $14,580 and $58,320 as an individual, or between $30,000 and $120,000 for a family of four.

2. Medicaid

If your income is low enough, Medicaid provides free or very low-cost health coverage. Eligibility varies by state.

3. Employer-Sponsored Insurance

If your employer offers group coverage, this almost always satisfies state mandate requirements at a lower cost to you.

4. Health Reimbursement Arrangements (HRAs)

Is It Illegal To Not Have Health Insurance? Individual Coverage HRAs let your company reimburse you for individual insurance premiums and medical bills. If you work for a small business with fewer than 50 employees, you might qualify for a Qualified Small Employer HRA (QSEHRA), which provides up to $6,350 for 2025 for individual coverage.

5. Short-Term Health Plans

These offer limited coverage and are less expensive, but they typically do not satisfy state mandate requirements. Use them only as a bridge between more comprehensive plans.

For a deeper look at your coverage options, visit the Insuranity Health Insurance Resource Hub, where complex topics like this are broken down for everyday readers.

A Quick Summary: Is It Illegal To Not Have Health Insurance?

| Situation | Legal Requirement? | Penalty Risk? |

|---|---|---|

| Federal level (all 50 states) | No mandate since 2019 | No federal penalty |

| California resident | Yes, state mandate | Up to $900+ per adult |

| Massachusetts resident | Yes, oldest state mandate | Based on income + age |

| New Jersey resident | Yes, state mandate | Based on income + family |

| Rhode Island resident | Yes, state mandate | $695+ per adult |

| Washington, D.C. resident | Yes, district mandate | $745+ per adult |

| Vermont resident | Yes, but no penalty | $0 penalty (currently) |

| All other 44 states | No legal requirement | No penalty |

FAQs

What is the penalty for not having health insurance in 2026?

In 2026, there is no federal penalty for being uninsured. However, certain states like California, Massachusetts, New Jersey, Rhode Island, and Washington D.C. may impose a state tax penalty, which can vary based on income, family size, and coverage gap duration.

Do immigrants or non-citizens need health insurance in the USA?

Health insurance requirements for immigrants depend on their residency status and the state they live in. Lawfully present immigrants may need coverage in mandate states, while undocumented immigrants are generally not eligible for federal programs but may access limited state-based healthcare options.

Can hospitals refuse treatment if you don’t have health insurance?

No, hospitals in the U.S. cannot refuse emergency treatment based on your insurance status under federal law. However, you may still receive a bill for the services provided, and non-emergency care may be denied or require upfront payment without insurance.

Is it cheaper to pay the penalty or buy health insurance?

In many cases, buying health insurance is more cost-effective than paying penalties and covering medical expenses out of pocket. Even basic plans can reduce financial risk significantly, while a single emergency without coverage can lead to thousands of dollars in unexpected costs.

Final Thoughts

So, is it illegal to not have health insurance? At the federal level, no. In five states and D.C., yes. Everywhere else, it is legal to go without coverage, but it is rarely wise.

Is It Illegal To Not Have Health Insurance? The bigger risk is not the tax penalty, it is the financial exposure that comes with one unexpected medical event. Health insurance is not just about following the law. It is about protecting yourself and your family from costs that can wipe out years of savings in a single afternoon.

At Insuranity, our mission is simple: turn confusing insurance rules into plain-English guides that anyone can act on. Whether you are exploring your first plan or trying to understand a penalty you received, we are here to walk you through it, step by step, state by state.

Disclaimer: This article is published by Insuranity for educational purposes only. Our goal is to translate complex insurance rules and legal topics into simple, easy-to-understand language for everyday readers. Nothing in this article should be taken as legal, financial, or tax advice. Laws and penalty amounts change over time and vary by state. Before making any decisions about your health coverage, please consult a licensed insurance professional, a certified tax advisor, or your state’s official health insurance marketplace. Insuranity is a research-based information guide. We educate, we do not recommend specific plans or actions for your personal situation.